Inventory Management: Techniques, EOQ & ABC Analysis

What is Inventory Management?

Inventory Management is the systematic approach to sourcing, storing, and selling inventory—both raw materials (inputs) and finished goods (products). In business, inventory is considered a necessary evil: too much ties up capital, but too little leads to lost sales.

Types of Inventory

Inventory in a business can be grouped into two main types: Direct Inventory and Indirect Inventory.

1. Direct Inventory

Direct inventory includes all items that are directly used to produce the final product.

These items become a physical part of the finished good.

Examples:

Direct raw materials (wood for furniture, steel for cars, cloth for shirts)

Direct components (tires in a bike, chips in a mobile phone)

Work-in-progress (partially manufactured goods)

Finished goods (ready for sale)

Meaning:

Direct inventory affects the cost of production directly.

2. Indirect Inventory

Indirect inventory includes materials that are not part of the final product, but are required to support production.

Examples:

Lubricants, oils, and coolants

Cleaning supplies

Machine tools and spare parts

Safety equipment (gloves, helmets)

Office supplies used in the factory

Indirect materials for maintenance

Meaning:

Indirect inventory supports production but does not become a part of the finished product.

Scope of Inventory Management

Inventory management covers all activities related to planning, controlling, and monitoring inventory. The scope includes:

1. Determining Inventory Levels

Deciding how much stock to keep so production runs smoothly without excess.

2. Setting Reorder Levels

Fixing the point at which a new order should be placed.

3. Selecting Inventory Control Techniques

Using methods like EOQ, ABC analysis, JIT, ROP, and Inventory Valuation Methods.

4. Managing Different Types of Inventory

Raw materials, work-in-progress (WIP), finished goods, and indirect materials.

5. Coordinating with Suppliers

Ensuring timely delivery, maintaining lead time, and building supplier relationships.

6. Avoiding Stockouts and Overstocking

Maintaining balance to prevent production stoppages or unnecessary storage costs.

7. Monitoring Inventory Performance

Using tools like Inventory Turnover Ratio to measure efficiency.

Key Objectives of Inventory Management

Operational Objectives

Ensure continuous flow of materials.

Prevent stockouts that can stop production.

Maintain smooth scheduling and production planning.

Financial Objectives

Minimize investment in inventory.

Reduce carrying (holding) costs.

Lower the total cost of inventory.

The Two Main Costs to Balance

1. Ordering Costs

Cost of placing an order: transportation, inspection, paperwork, and handling.

Ordering cost decreases when ordering large quantities less often.

2. Carrying (Holding) Costs

Cost of storing inventory: rent, insurance, deterioration, obsolescence, and theft.

Holding cost increases when inventory is stored in large quantities.

Goal of Inventory Management:

Minimize Total Inventory Cost

(Total Inventory Cost = Ordering Cost + Carrying Cost)

Importance of Inventory Management

1. Ensures Uninterrupted Production

Prevents delays caused by shortage of materials.

2. Reduces Overall Costs

Controls ordering and holding costs, improving profitability.

3. Improves Customer Satisfaction

Ensures products are available when customers need them.

4. Better Use of Warehouse Space

Avoids excess stock and makes storage more efficient.

5. Helps in Accurate Financial Reporting

Proper valuation affects profit, cost of goods sold, and the balance sheet.

6. Enhances Supplier Relations

Timely orders and clear planning lead to stronger supply chain coordination.

7. Supports Decision Making

Data on stock movement helps managers improve forecasting and production planning.

Techniques of Inventory Control

Managers use several techniques and mathematical models to maintain the right amount of inventory and avoid shortage or excess.

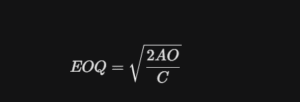

1. Economic Order Quantity (EOQ)

Concept:

EOQ helps find the ideal order size that minimizes both ordering cost and carrying cost.

Formula:

A = Annual Usage/Demand (units)

O = Ordering Cost per order

C = Carrying Cost per unit per year

Example: If Annual Demand = 2000 units, Ordering Cost = ₹50, Carrying Cost = ₹25.

2. Reorder Point (ROP) & Safety Stock

Concept: When should you place the next order? You don’t wait until stock hits zero. You order when stock reaches the Reorder Level.

Formula:

Lead Time: The time taken by the supplier to deliver goods after receiving the order.

Safety Stock (Buffer Stock): Extra stock kept to protect against stockouts during emergencies.

3. ABC Analysis (Always Better Control)

Concept: Not all inventory items are equally important. This technique classifies items based on their usage value to prioritize control. It follows the Pareto Principle (80/20 rule).

A-Items (High Value): 70-80% of total value, but only 10-20% of quantity. Action: Strict control, low safety stock, frequent ordering.

B-Items (Moderate Value): 15-20% value, 30% quantity. Action: Moderate control.

C-Items (Low Value): 5-10% value, 50% quantity. Action: Loose control, bulk ordering (e.g., nuts and bolts).

Purchasing Methods: Centralized vs. Decentralized

How a company buys materials affects its efficiency.

| Feature | Centralized Purchasing | Decentralized Purchasing |

| Definition | One central Head Office buys for all branches/plants. | Each branch/department buys its own materials independently. |

| Price | Low: Bulk buying gets heavy discounts. | High: Smaller orders mean higher prices. |

| Control | High: Uniform policies and better control. | Low: Harder to monitor total spend. |

| Speed | Slow: Can be bureaucratic and delay delivery. | Fast: Quick response to local needs. |

| Suitability | Organizations with similar needs across units. | Geographically separated units with diverse needs. |