What is Working Capital Management? (Concept & Meaning)

Working Capital Management is the functional area of finance that deals with a firm’s current assets and current liabilities. It ensures the company has sufficient liquidity to run day-to-day operations while maximizing profitability.

Working Capital refers to funds invested in current assets like raw materials, work-in-progress, finished goods, debtors, and cash.

Two Concepts of Working Capital:

Gross Working Capital: The total investment in all current assets.

Net Working Capital: The excess of total current assets over total current liabilities.

Formula:Net Working Capital = Current Assets - Current Liabilities

Types based on Time:

Permanent (Hard Core) Working Capital: The minimum level of current assets required at all times to carry out business. It should ideally be financed by long-term sources.

Temporary (Variable) Working Capital: The additional capital required over and above the permanent level to meet fluctuating demands (e.g., seasonal spikes).

The Working Capital Cycle (Operating Cycle)

The Operating Cycle refers to the length of time from the purchase of raw materials to the realization of cash from sales. It represents the time funds are tied up in the business process.

Formula:Operating Cycle = R + W + F + D - C

R = Raw Material Storage Period

W = Work-in-Progress Holding Period

F = Finished Goods Storage Period

D = Debtors Collection Period

C = Credit Period from Suppliers

Getty Images

Note: A shorter operating cycle means the firm needs less working capital because cash is recovered quickly. A longer cycle requires more working capital.

Approaches to Financing Working Capital

How should a firm fund its working capital needs? There are three main approaches based on the risk-return trade-off.

1. Matching (Hedging) Approach

The firm matches the maturity of the source of funds with the life of the asset.

Long-term sources finance Fixed Assets + Permanent Working Capital.

Short-term sources finance Temporary Working Capital.

Risk/Return: Moderate.

2. Conservative Approach

The firm relies more on long-term funds to be safe.

Long-term sources finance Fixed Assets + Permanent Working Capital + Part of Temporary Working Capital.

Short-term sources finance only the remaining peak temporary needs.

Risk/Return: Low Risk (high liquidity), but Lower Return (since long-term funds are costlier).

3. Aggressive Approach

The firm relies heavily on short-term funds to save costs.

Short-term sources finance Temporary Working Capital + Part of Permanent Working Capital.

Risk/Return: High Risk (danger of insolvency if loans aren’t renewed), but Higher Return (since short-term funds are cheaper).

Shutterstock

Regulation of Bank Finance (Tandon Committee)

Banks are the primary source of working capital finance in India. To regulate this, the RBI set up the Tandon Committee (1974) to introduce financial discipline.

The 3 Methods of Lending (Maximum Permissible Bank Finance – MPBF):

Method 1: Bank lends 75% of the Working Capital Gap (Current Assets – Current Liabilities). The borrower provides 25% from long-term sources.

Formula:MPBF = 0.75 (CA - CL)

Method 2: Bank lends 75% of Total Current Assets minus Current Liabilities. The borrower provides 25% of Total Current Assets.

Formula:MPBF = (0.75 * CA) - CL

Method 3: Bank lends against “Core Current Assets.” (Rarely used).

Impact: These norms ensured that companies maintain a minimum current ratio and do not rely entirely on bank funds for their operations.

Factors Affecting Working Capital Needs

Nature of Business: Manufacturing firms need more WC than trading or service firms due to production cycles.

Production Policy: Seasonal vs. steady production affects inventory levels.

Credit Policy: Liberal credit to customers increases debtors, increasing WC needs.

Business Cycle: Booms increase demand and WC needs; recessions decrease them.

Growth & Expansion: Growing firms need more WC for larger operations.

The Time Value of Money (TVM) is one of the most important concepts in finance. It states that money available today is worth more than the same amount in the future because it has the potential to earn interest.

Why is money today more valuable?

Because you can invest money now and earn a return and everything else in future is uncertain. Interest is the reward for waiting or the cost of borrowing money.

Important Terms

Principal (P): The original amount of money invested or lent.

Interest Rate (i): The percentage charged or earned per time period (e.g., 6% per year).

Time (n): Number of periods the money is invested.

Future Value (FV): Amount an investment grows to in the future.

Present Value (PV): Current value of a future amount.

Future Value (Compounding)

Future Value tells us how much an investment made today will be worth in the future.

1. Simple Interest

Interest is earned only on the original principal.

SimpleInterest= Principal × Rate × Time

2. Compound Interest

Interest is earned on principal + previous interest (the power of compounding).

Formula: Future Value of a Single Amount

FV = PV (1 + i)^n

Where:

FV = Future Value

PV = Present Value

i = Interest Rate per period

n = Number of periods

Note: More frequent compounding (monthly/quarterly) results in a higher future value.

Present Value (Discounting)

Present Value is the current worth of a future sum of money.

It answers:

How much should I invest today to receive ₹X in the future?

Formula

PV = FV / (1 + i)^n

Example on Present value of Money

Alpha Company can invest at 16% interest compounded annually, while Beta Company can invest at 16% interest compounded semi-annually. Both companies need ₹2,00,000 after 4 years. We will calculate how much each must invest today (Present Value).

Beta Company needs to invest less today because its investment grows faster due to more frequent compounding.

Annuities (Series of Equal Payments)

An annuity is a series of equal payments made at regular intervals of time (e.g., rent, insurance, pension).

1. Future Value of an Ordinary Annuity

The value of all future payments plus interest earned.

FV_annuity = R × [((1 + i)^n – 1) / i]

Where R = periodic payment (rent)

2. Present Value of an Ordinary Annuity

The lump sum needed today to provide equal future payments.

PV_annuity = R × [(1 – (1 + i)^(-n)) / i]

Example: Future Value of an Ordinary Annuity

In the beginning of 2006, the directors of Molloy Corporation decided that the plant facilities must be expanded in a few years. The company plans to invest ₹50,000 every year, starting on June 30, 2006, into a trust fund that earns 11% interest compounded annually.

Question

How much money will be in the fund on June 30, 2010, after the last deposit has been made?

Solution

The first deposit is made at the end of the first year, so it is an ordinary annuity

Number of periods (n) = 5 years

Interest rate (i) = 11%

The last deposit (2010) earns no interest because it is deposited on the final day

From the Future Value of Ordinary Annuity Table, Future Value Factor (at n = 5, i = 11%) = 6.22780

Formula

FV = Rent × Future Value Annuity Factor

Calculation

FV = 50,000 × 6.22780 FV = ₹3,11,390

Conclusion

Molloy Corporation will have ₹3,11,390 in the fund on June 30, 2010.

Finding the Required Annual Deposit

If the company needs exactly ₹3,00,000 on June 30, 2010, how much must it deposit every year?

Formula

Rent = FV / Future Value Annuity Factor

Calculation

Rent = 3,00,000 / 6.22780 Rent = ₹48,171.10

Final Answer

The company must deposit ₹48,171 every year to accumulate ₹3,00,000 by June 30, 2010.

Perpetuities

A Perpetuity is an annuity that pays forever (infinite life). Examples: perpetual bonds, preferred stock dividends.

Formula

PV = C / i

Where C = constant annual payment

Growth Calculations & Doubling Money

1. Compound Annual Growth Rate (CAGR)

gr = (Vn / V0)^(1/n) – 1

2. Rule of 72

A shortcut to estimate how long it takes to double money.

Finance is the art and science of managing money. Virtually all individuals and organizations earn, raise, spend, or invest money. Financial Management is broadly concerned with the acquisition and use of funds by a business firm.

In earlier years, it was synonymous with just raising funds. Today, its scope has broadened to include the efficient use of resources.

Scope of Financial Management

Financial management focuses on managing money in a smart and planned way. Its main aim is to make sure the business has enough funds and uses them correctly to increase profit and value. The scope of financial management includes the following areas:

1. Financial Analysis, Planning & Control

It means understanding the company’s financial position by analyzing financial statements like Balance Sheet & Profit-Loss account.

Planning helps decide how much money is required and where it will be spent.

Control ensures that money is used properly and not wasted.

Example: Checking budgets, comparing actual performance with planned performance.

2. Profit Planning

Profit planning means deciding the expected level of profit and making strategies to achieve it.

It includes controlling costs, increasing sales, and improving efficiency.

Example: Setting profit targets for the year and preparing plans to reach them.

3. Financial Forecasting

It means predicting the future financial needs of the business.

Helps in estimating cash needs, investment requirements, and financial risks.

Example: Forecasting future sales, future expenses, and capital needs.

4. Acquisition and Use of Funds

It means arranging funds from different sources (like shares, loans, debentures).

Also includes deciding where and how to invest this money to earn the best return.

Example: Raising money from the bank and investing it to buy new machinery.

Objectives: Profit Maximization vs. Wealth Maximization

Every Finance Manager has to ask one question: “What is our ultimate goal?”

There are two schools of thought: the Traditional approach (Make Profit) and the Modern approach (Create Wealth).

1. Profit Maximization (The Old School)

The Idea:

Business exists to make money. Therefore, any decision that increases profit is “Good,” and any decision that reduces profit is “Bad.”

Why it sounds right: It’s simple. Profit measures efficiency. If we are profitable, we survive.

Why it is actually WRONG (The Flaws):

It is Vague: What is “Profit”? Is it short-term profit? Long-term? Before tax? After tax? It is not clear.

Ignores Risk:

Example: Project A gives a guaranteed profit of ₹50,000. Project B gives a profit of ₹1 Lakh but has a 50% chance of failing completely.

A “Profit Maximizer” would choose Project B because the profit is higher, ignoring the huge risk of losing everything.

Ignores Time Value of Money:

Example: Option A gives you ₹1 Lakh today. Option B gives you ₹1 Lakh after 5 years.

Profit Maximization says both are equal (₹1 Lakh = ₹1 Lakh). But common sense tells us money today is more valuable than money 5 years later.

2. Wealth Maximization (The Modern School)

The Idea:

The goal is not just to earn profit, but to increase the Market Value of the company. This is also called Shareholder Value Maximization. The focus is on increasing the share price in the stock market.

The Formula:

Wealth = Number of Shares Owned × Current Market Price per Share

Why it is BETTER:

Considers Risk: It avoids risky projects because high risk makes share prices fall.

Considers Time: It recognizes that cash now is better than cash later. It uses Discounted Cash Flow (DCF) techniques.

Long-Term Focus: It doesn’t cut corners to make a quick buck. It invests in quality, brand, and research, which increases the company’s value over 10-20 years.

Considers Everyone: To keep the share price high, a company must treat customers, employees, and society well. If they cheat customers to make a quick profit, the share price will eventually crash.

Comparison: Which one wins?

Basis

Profit Maximization

Wealth Maximization

Concept

Traditional / Narrow

Modern / Broad

Goal

Earn large profits

Increase market value of shares

Time Horizon

Short-term focus

Long-term focus

Risk

Ignores risk factor

Considers risk factor

Time Value

Ignores timing of returns

Recognizes money has time value

Best For

Survival stage companies

Established, growing companies

While Profit is necessary for survival (like oxygen), Wealth Maximization is the ultimate goal (like a healthy life). A good Financial Manager always chooses Wealth Maximization because it accounts for risk, time, and future growth.

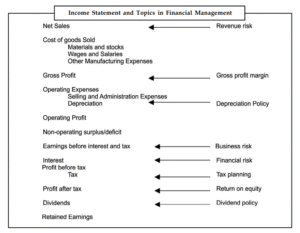

The Three Key Finance Functions (Decisions)

Financial management revolves around three major decisions that must be optimal to maximize firm value.

1. Investment Decision

Where should the firm invest its funds?

Capital Budgeting: Selecting long-term assets (projects) that yield returns in the future.

Working Capital Management: Managing current assets (cash, receivables, inventory) for day-to-day operations.

2. Financing Decision

How should the firm raise funds?

Capital Structure: Determining the right mix of Debt and Equity.

Source of Funds: Choosing between loans, shares, or retained earnings based on cost and risk.

3. Dividend Decision

How much profit should be distributed among stakeholders?

Dividends: Distributing profits to shareholders.

Retained Earnings: Keeping profits for reinvestment in the company.

The manager must decide the optimal dividend payout ratio that maximizes shareholder wealth.

Shutterstock

Interface of financial management with Other Functions

Finance is the lifeblood of an organization and connects with all other departments:

Marketing: Finance allocates budget for ads and sales campaigns.

Production: Finance approves funds for machinery and raw materials.

HR: Finance manages payroll and benefits costs.

Economics: Financial managers use economic theories (supply-demand, marginal analysis) for efficient operations.

Accounting: While accountants focus on accrual-based reporting, financial managers focus on cash flows for decision-making.

Understanding Capitalization

Before we jump into “Over” or “Under,” let’s understand Capitalization.

In simple terms, Capitalization is the total amount of money invested in the business (Shares + Debentures + Long-term Loans).

Think of capitalization like a shirt.

Fair Capitalization: The shirt fits perfectly. The capital invested generates just the right amount of profit.

Overcapitalization: The shirt is too loose (Too much capital, too little profit).

Undercapitalization: The shirt is too tight (Too little capital recorded, but massive profit).

1. Overcapitalization

A company is Overcapitalized when it has raised more money than it can profitably use. It sounds like having “too much money,” but in finance, it is a bad situation.

Simple Definition:

When a company’s earnings are very low compared to the huge capital it has invested. It is like buying a Ferrari just to deliver pizzas—the investment is huge, but the return is tiny.

Example:

Imagine Company A invests ₹10 Lakhs. The normal industry return is 10% (so it should earn ₹1 Lakh). However, Company A only earns ₹50,000.

The shareholders invested a lot but are getting very little return.

Verdict: Company A is Overcapitalized.

Symptoms (How to spot it):

Low Dividend: The company cannot pay good dividends because profits are low.

Low Share Price: Since dividends are low, people sell the shares, and the market price falls below the face value (e.g., a ₹10 share trades at ₹8).

Difficulty Raising Loans: Banks won’t lend money because the company isn’t profitable enough.

Causes (Why it happens):

Buying assets at high prices: Buying machinery when it was very expensive.

High Promotion Costs: Spending too much money on ads that didn’t bring sales.

Liberal Dividends: In the past, the company distributed all profits to shareholders and didn’t save anything for the future.

Remedies (How to fix it):

Reduction of Capital: Cancel old shares and issue new ones at a lower value.

Buyback: The company buys back its own shares to reduce the number of claimants on profit.

2. Undercapitalization

A company is Undercapitalized when it has very little recorded capital but is making huge profits. This sounds good, but it has dangerous side effects.

Simple Definition:

When a company’s earnings are exceptionally high compared to the capital invested. It is like a small roadside stall making crores in profit.

Example:

Imagine Company B invests only ₹1 Lakh. The normal industry return is 10% (expected profit ₹10,000). But Company B earns ₹50,000 (a 50% return!).

The return is massive compared to the small investment.

Verdict: Company B is Undercapitalized.

Symptoms (How to spot it):

High Dividend: The company pays huge dividends.

High Share Price: Everyone wants to buy these shares, so the market price shoots up above book value (e.g., a ₹10 share trades at ₹50).

High Secret Reserves: The company has a lot of hidden profit saved up.

Causes (Why it happens):

Buying assets cheaply: Buying a factory during a recession (low price) which is now producing great value.

Conservative Policy: For years, the company saved its profits instead of distributing them, making the company internally very rich.

High Efficiency: The management is super efficient and generates profit out of nothing.

Consequences (The hidden dangers):

Competition: Seeing huge profits, rivals will enter the market to copy you.

Labor Trouble: Workers will demand higher wages seeing the high profits.

Consumer Anger: Customers might feel the company is overcharging them to make such high profits.

Remedies (How to fix it):

Stock Split: Divide 1 share of ₹100 into 10 shares of ₹10. This reduces the earnings per share to look normal.

Bonus Shares: Issue free shares to existing shareholders to convert savings into capital.

Feature

Overcapitalization (Bad)

Undercapitalization (Risky but Good)

Earnings

Very Low

Very High

Share Price

Lower than Face Value

Higher than Face Value

Real Value

Assets are worth less than recorded.

Assets are worth more than recorded.

Remedy

Reduce Capital / Buyback

Issue Bonus Shares / Stock Split

Conclusion:

Financial management is more than just procurement of funds. It is about the optimal combination of investment, financing, and dividend decisions to maximize the wealth of shareholders while maintaining ethical standards and stakeholder relationships.

“Financial Management” is often considered the backbone of the BBA curriculum and appears in the 3rd Semester of exams. This subject moves from simple accounting to teach you the methodologies of decision-making: How do companies decide where to invest? How do they raise money? How do they manage cash?

Lu notes has organized the complete syllabus into easy-to-understand notes to help you master these calculations and concepts. Just click on your desired topic below to access the notes!

Unit 1: Introduction & Investment Decisions

This unit covers the basics of finance and the crucial tools for deciding long-term investments.

Introduction to Financial Management: Concept, Functions, Objectives, Profitability vs. Shareholder Wealth Maximization [View Notes]

Time Value of Money- Compounding & Discounting [View Notes]

Investment Decisions: Capital Budgeting (Payback, NPV, IRR, ARR) [View Notes]

Unit 2: Financing Decisions

This unit focuses on how companies raise funds and the cost associated with those funds.

Consequences and Remedies of Over and Under Capitalization (I have already explained this topic in the first article “Introduction to Financial Management.” Please visit that article, and you will find the detailed explanation below in that post.

Cost of Capital & WACC (Weighted Average Cost of Capital) [View Notes]

Determinants of Capital Structure [View Notes]

Capital Structure Theories [View Notes]

Unit 3: Dividend Decisions

This unit explores how companies decide how much profit to keep and how much to give back to shareholders.

Dividend Decision: Concept and Relevance [View Notes]

Dividend Models: Walter’s Model [View Notes]

Dividend Models: Gordon’s Model [View Notes]

Dividend Models: MM Hypothesis (Modigliani-Miller) [View Notes]

Dividend Policy and its Determinants [View Notes]

Unit 4: Working Capital Management

The final unit deals with the day-to-day financial health of a business.

Management of Working Capital: Concepts & Approaches [View Notes]

Management of Cash [View Notes]

Management of Receivables [View Notes]

Management of Inventory [View Notes]

CREDIT : Shutterstock

📚 Keep Studying!

We hope these Financial Management notes help you master the numbers and ace your exams. LuNotes is your one-stop solution for all Lucknow University notes. Don’t forget to check out our notes for other subjects in your semester!

[Link to Marketing Management Notes]

[Link to Human Resource Management Notes]

[Link to Operations Management Notes]

Found a mistake? We work hard to ensure all notes are 100% accurate and as per the latest LU syllabus. If you spot an error, find a missing subject, or have a request, please [click here to let us know]! (You can link this text to your contact page or WhatsApp).

By LuNotes – your trusted for Lucknow University Semester exam notes, crafted with love. ❤️

Capital Budgeting is the planning process used by firms to evaluate and select major longterm investments. These decisions involve large expenditures on fixed assets like buying new machinery, constructing a factory or developing a new product.

It results in a Capital Budget—the firm’s formal plan for its outlay on fixed assets.

Why is Capital Budgeting Important?

Affects Profitability: A good investment can yield spectacular returns, while a bad one can endanger the firm’s survival.

Long-Term Effects: The impact of these decisions is felt over many years (e.g., a new factory changes the cost structure for decades).

Irreversibility: Once made, these decisions are hard to reverse without huge financial loss.

Huge Investment: It involves substantial capital, ranging from thousands to crores of rupees.

Scarcity of Resources: Capital is limited. Firms must choose the best project among many options.

🔄 The Capital Budgeting Process

A capital budgeting decision is a two-sided process:

Calculate Expected Return: Estimating the cash outflows (costs) and the stream of future cash inflows (benefits).

Select Required Return: Determining the minimum return the project must earn to be acceptable (based on risk).

Critical Rules for Estimating Cash Flows

Only Cash Flow Matters: We look at actual cash, not accounting profit. To find Cash Inflow, we add non-cash expenses (like depreciation) back to the profit after tax.

Cash Inflow = Profit After Tax + Depreciation

Ignore Sunk Costs: Money already spent in the past is irrelevant.

Include Opportunity Costs: If a project uses a resource you already own, the money you could have earned by selling or renting it is a cost.

Consider Working Capital: Projects often require extra inventory or cash on hand. This is an initial outflow and a final inflow when the project ends.

Ignore Interest: Do not deduct interest payments when estimating cash flows; the cost of capital (discount rate) accounts for this.

📊 Techniques for Evaluation: Traditional vs. Discounted

There are two main categories of techniques used to evaluate investment proposals.

A. Traditional Techniques (Non-Discounted)

These methods are simple but ignore the time value of money (i.e., they assume ₹1 today is worth the same as ₹1 in five years).

1. Payback Period Method

This determines how long it takes for a project to recover its initial investment cost.

Formula:Payback Period = Cost of Project / Annual Cash Inflow

Decision Rule: Accept the project with the shorter payback period.

🧮 Numerical Example: Payback Period

Problem: A project costing ₹20 Lakhs yields an annual profit of ₹3 Lakhs after depreciation (@12.5% SLM) but before tax (50%). Calculate the Payback Period.

Solution:

First, we must find the Annual Cash Inflow.

Depreciation: Let’s assume depreciation is ₹2,00,000.

Profit Before Tax: ₹3,00,000

Less Tax (50%): ₹1,50,000

Profit After Tax: ₹1,50,000

Add Back Depreciation: + ₹2,00,000 (Because it’s a non-cash expense)

Annual Cash Inflow:₹3,50,000(Note: The text example used ₹4,00,000 as the final inflow figure to arrive at 5 years. Let’s use the text’s final figures for clarity).

This is a simple method to estimate the internal rate of return. It is calculated as 1 ÷ Payback Period.

🧮 Numerical Example:

Initial Cash Outlay: ₹2,00,000

Annual Cash Savings: ₹50,000

Payback Period = 2,00,000 / 50,000 = 4 Years

Payback Reciprocal = 1 / 4 = 25%

3. Accounting Rate of Return (ARR)

This method uses accounting profit (not cash flow) to calculate return on investment.

Formula:ARR = (Average Annual Profit / Average Investment) x 100

Limitations: Ignores time value of money; based on accounting profits which can be manipulated.

B. Discounted Cash Flow (DCF) Techniques

These methods are superior because they consider the Time Value of Money. They discount future cash flows to their Present Value (PV) using a specific interest rate (Cost of Capital).

4. Net Present Value (NPV)

This is the most reliable method. It calculates the total present value of all future cash inflows minus the initial cash outflow.

Decision Rule: If NPV > 0, Accept the project (It adds value to the firm).

🧮 Numerical Example: NPV

Problem: JP Company wants to buy a machine costing ₹33,522. It will generate annual cash savings of ₹10,000 for 5 years. The company’s cost of capital is 12%.

Solution:

We need to find the Present Value (PV) of the 5 annual payments of ₹10,000.

PV Factor for annuity of 5 years @ 12% = 3.605

Calculation Step

Value (₹)

PV of Cash Inflows (10,000 × 3.605)

36,050

Less: PV of Cash Outflows (Cost)

(33,522)

Net Present Value (NPV)

2,528

Conclusion: Since the NPV is positive (₹2,528), the project is acceptable.

5. Profitability Index (PI)

Also called the Desirability Factor. It measures the ratio of benefits to costs.

Formula:PI = PV of Cash Inflows / PV of Cash Outflows

Decision Rule: Accept if PI > 1.

6. Internal Rate of Return (IRR)

This is the exact discount rate that makes the NPV equal to zero. It represents the project’s actual rate of return.

Decision Rule: Accept if IRR > Cost of Capital.

🚧 Capital Rationing

Sometimes, a firm has more profitable projects than it has money to fund. This is called Capital Rationing. The goal is to select the combination of projects that fits within the budget and maximizes value.

🧮 Numerical Example: Capital Rationing

Problem: S. Ltd. has ₹10,00,000 allocated. Which projects should they choose?

Project

Investment (₹)

Profitability Index (PI)

1

3,00,000

1.22

2

1,50,000

0.95

3

3,50,000

1.20

4

4,50,000

1.18

5

2,00,000

1.20

6

4,00,000

1.05

Solution:

Rank projects by PI (highest to lowest) and select until the budget is full.

Rank 1: Project 1 (PI 1.22) – Cost ₹3,00,000

Rank 2: Project 3 (PI 1.20) – Cost ₹3,50,000

Rank 3: Project 5 (PI 1.20) – Cost ₹2,00,000

Total Cost so far: ₹8,50,000

Remaining Budget: ₹1,50,000

Next Best: Project 4 (PI 1.18) costs ₹4,50,000. We cannot afford it.

Optimal Combination: Projects 1, 3, and 5.

⚠️ Dealing with Risk in Capital Budgeting

Risk refers to the chance that a project will prove unacceptable (NPV < 0).

Ever heard the saying, “a rupee today is worth more than a rupee tomorrow”? That’s the single most important idea in all of finance. It’s called the Time Value of Money (TVM), and mastering it is essential for your BBA or MBA exams and your future career.

But what does it really mean?

Simply put, money you have right now is more valuable than the exact same amount in the future. Why? Because you can invest it. That ₹100 you have today could be put in a bank to earn interest, turning it into ₹105 by next year.

This article will break down all the core TVM concepts, formulas, and examples you need to know.

1. Simple vs. Compound Interest: The Two Ways Money Grows

First, let’s understand interest. It’s the fee you pay for borrowing money or the reward you get for saving it. The starting amount is called the Principal (P). (the amount which you give to the bank and gets interest onto it)

What is Simple Interest?

Simple interest is the most basic form. It’s calculated only on the original principal amount.

Simple Interest Formula:Interest = P * i * n

P = Principal

i = Interest rate

n = Number of time periods

Example: You lend ₹10,000 at 3% simple interest per quarter.

Interest per quarter: ₹10,000 * 0.03 * 1 = ₹300

Total interest over 5 years (20 quarters): ₹300 * 20 = ₹6,000

What is Compound Interest?

This is where the magic happens. Compound interest is calculated on the principal plus all the interest you’ve already earned. You start earning “interest on your interest.”

Example: You invest ₹1,000 at 6% interest compounded annually.

End of Year 1: ₹1,000 * 1.06 = ₹1,060

End of Year 2: ₹1,060 * 1.06 = ₹1,123.60

Notice you earned ₹63.60 in year 2, not just ₹60. That extra ₹3.60 is 6% interest on the ₹60 you earned in year 1.

Key Takeaway: The more frequently interest is compounded (e.g., monthly vs. annually), the faster your money grows.

2. Future Value (FV): What Will Your Money Be Worth?

Future Value (FV) tells you what a single amount of money today will be worth at a specific point in the future. This process is called compounding.

This answers the question: “If I invest ₹X today, how much will I have in 5 years?”

Future Value Formula (for a Single Amount)

FV = P * (1 + i)^n

FV = Future Value

P = Principal (or Present Value)

i = Interest rate per period

n = Number of periods

FV Example

Problem: A company invests ₹40,00,000 for 5 years at 16% per year, compounded semi-annually. What is the future value?

Solution:

P: ₹40,00,000

i: 16% / 2 = 8% per period (0.08)

n: 5 years * 2 periods per year = 10 periods

Calculation:FV = 40,00,000 * (1 + 0.08)^10

FV = ₹86,35,680

3. Present Value (PV): What is Future Money Worth Today?

Present Value (PV) is the exact opposite of FV. It tells you what a future amount of money is worth in today’s terms. This process is called discounting.

This answers the question: “I need to have ₹5,00,000 in 10 years. How much do I need to invest today to get there?”

Present Value Formula (for a Single Amount)

PV = FV / (1 + i)^n

PV = Present Value

FV = Future Value (the amount you want in the future)

i = Discount rate (interest rate) per period

n = Number of periods

PV Example

Problem: You need ₹2,00,000 in 4 years. How much must you invest today if the interest rate is 16% compounded semi-annually?

Solution:

FV: ₹2,00,000

i: 16% / 2 = 8% per period (0.08)

n: 4 years * 2 periods per year = 8 periods

Calculation:PV = 2,00,000 / (1 + 0.08)^8

PV = ₹108,054

This means ₹108,054 invested today at 8% per period will grow to ₹2,00,000 in 4 years.

4. Annuities: The Power of Equal Payments

An Annuity is simply a series of equal payments made at equal time intervals. Think of a car loan, a mortgage payment, or a regular monthly saving plan.

Ordinary Annuity: Payments are made at the end of each period (this is the most common type).

Future Value of an Annuity (FVA)

This tells you the total value of a stream of regular payments at a future date.

Formula:FVA = R * [((1 + i)^n - 1) / i]

R = Rent (the amount of each equal payment)

Example: You invest ₹50,000 every year for 5 years in a fund that earns 11% annually. How much will you have at the end?

The Cost of Capital is a central concept in financial management and a cornerstone of modern finance theory. In simple terms, it is the minimum rate of return that a company must earn on its investments to maintain the market value of its shares.

Think of it as the “hurdle rate” that a new project must clear. If a project is expected to earn a return of 12%, but the company’s cost of capital is 14%, accepting the project would actually destroy value for the company’s investors. The cost of capital is expressed as a percentage (%).

It can be viewed from three different angles:

From an Investor’s Viewpoint: It’s the measure of the sacrifice made by investing in a company instead of somewhere else (like a bank deposit).

From a Firm’s Viewpoint: It’s the minimum required rate of return needed to justify raising and using capital.

From a Capital Expenditure Viewpoint: It’s the “cut-off rate” or discount rate used to value the future cash flows of a project.

Why is the Cost of Capital So Important? 🎯

The concept of cost of capital is vital for several key financial decisions.

Investment Evaluation (Capital Budgeting): The cost of capital is the primary financial standard used to evaluate long-term investment projects. In the Net Present Value (NPV) method, it’s used as the discount rate to calculate the present value of future cash inflows. In the Internal Rate of Return (IRR) method, a project is only accepted if its IRR is greater than the cost of capital.

Designing the Capital Structure: This concept helps a firm design a sound and economical capital structure, which is its mix of debt and equity. The goal is to find the optimal mix that minimizes the overall cost of capital and maximizes the value of the firm.

Appraising Financial Performance: The cost of capital framework can be used to evaluate the financial performance of top management. This involves comparing the actual profitability of investment projects with the company’s overall cost of capital.

The Building Blocks: Calculating Specific Costs

A company raises funds from various sources, such as equity shares, preference shares, debentures (debt), and retained earnings. The financial manager must compute the specific cost of each type of fund.

Cost of Debt (Kd)

Debt capital is raised through debentures or loans from financial institutions. The interest paid on debt is a tax-deductible expense, which means the government effectively subsidizes a portion of it. Therefore, the cost of debt is always calculated on an after-tax basis.

For Irredeemable (Perpetual) Debt:

Kd=NPI(1−t)

Where I is the annual interest, t is the corporate tax rate, and NP is the net proceeds from the debenture issue.

Cost of Preference Shares (Kp)

Preference shares have a fixed dividend rate, but unlike debt interest, these dividends are paid out of after-tax profits and are not tax-deductible.

For Irredeemable Preference Shares:

Kp=NPD

Where D is the annual preference dividend and NP is the net proceeds from the share issue.

Cost of Equity (Ke)

This is the most difficult cost to measure because there is no fixed payment promised to equity shareholders. The cost of equity is the minimum rate of return a firm must earn on its equity-financed projects to keep the market price of its shares unchanged. The most common method to calculate it is the Dividend Growth Model.

Dividend Price plus Growth Rate Approach: This model assumes that dividends will grow at a constant rate (g) forever.

Ke=NPD1+g

Where D1 is the expected dividend per share next year, NP is the net proceeds per share, and g is the constant growth rate in dividends.

Cost of Retained Earnings (Kre)

Retained earnings are profits that the company keeps instead of paying out as dividends. These are not “free” funds; they have an opportunity cost. This is because the shareholders could have received that money as dividends and invested it elsewhere. Therefore, the cost of retained earnings is the return shareholders forgo, and it is generally considered to be the same as the cost of equity (Ke).

Putting It All Together: Weighted Average Cost of Capital (WACC)

The Weighted Average Cost of Capital (WACC) is the composite or overall cost of capital for a firm. It is an average of the specific costs of each source of funds, weighted by the proportion they hold in the firm’s capital structure.

How to Calculate WACC

Determine the funds to be raised from each source and their proportion.

Compute the specific cost of each source of funds.

Assign weights to each specific cost.

Multiply the cost of each source by its weight.

Sum up all the weighted costs to get the WACC.

Assigning Weights: Book Value vs. Market Value

A crucial step is deciding how to assign weights.

Book Value Weights: These are based on the accounting values found on the company’s balance sheet. They are simple to calculate and readily available but are based on historical costs, which may not reflect current economic reality.

Market Value Weights: These are based on the current market prices of the company’s securities. This method is theoretically sound and preferred by most financial analysts because it reflects current values and is consistent with the goal of maintaining market value. However, market values can be volatile and may not be available for unlisted companies.

What is Marginal Cost of Capital?

The marginal cost of capital is the cost of raising additional or new funds required by a firm for an expansion or new project. It’s the weighted average cost of this new, incremental capital. It can be different from the overall WACC if the financing mix or component costs change for the new funds.

Factors that Influence WACC ⚖️

A company’s WACC is influenced by both internal and external factors.

Controllable Factors

These are factors the firm’s management can control:

Capital Structure Policy: The company’s choice of debt and equity mix directly affects its WACC.

Dividend Policy: The decision to retain earnings or pay them out as dividends affects how new equity capital is raised.

Investment Policy: Investing in projects with different risk profiles than existing assets can change the firm’s overall risk and its cost of capital.

Uncontrollable Factors

These are external factors the firm cannot control:

Tax Rates: Changes in corporate tax rates directly affect the after-tax cost of debt.

Level of Interest Rates: The overall level of interest rates in the economy is a primary driver of the cost of debt.

Market Risk Premium: This is the extra return investors demand for investing in the stock market over risk-free assets, and it’s determined by general market sentiment.